At SnapShot, we aim to empower traders and anyone engaged in Futures and Forex trading with an advanced statistical analysis tool, backed by an extensive historical database, and a user-friendly interface. Our platform is designed to facilitate data driven decisions, harnessing the power of statistical analysis against the first hour of the session to provide you with the insights necessary to make informed and effective trading decisions.

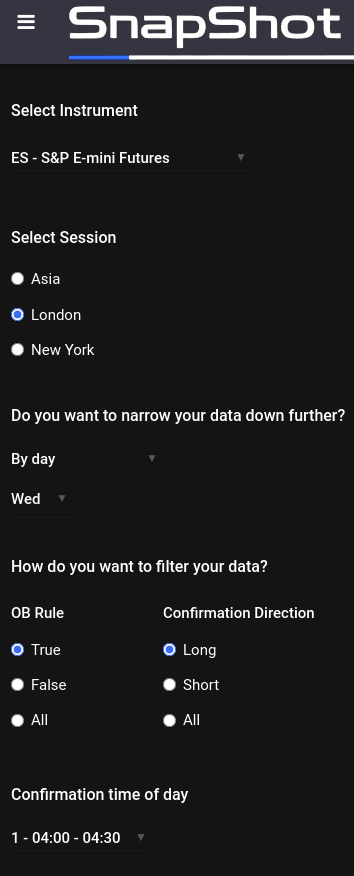

Filtering

This is the filtering sidebar, your control panel for streamlining and targeting data. This allows you to conduct multilevel filtering for precise data querying and statistical analysis.Start by selecting the ‘Instrument’ of interest. Followed by the ‘Session’ you are trading.Further granularity can be achieved with the period filters: ‘By day’, ‘By Month’, and ‘By week of month’. These allow you to concentrate your analysis on specific timeframes.Once the filter period is set, refine your data search with the ‘OB Rule’ filter. This feature provides options for ‘true’, ‘false’, or ‘all’, enabling you to customize the data depending on current market conditions.The ‘Confirmation Direction’ filter then offers you the ability to specify the market direction as ‘long’, ‘short’, or ‘all’.To wrap up the filtering process, the ‘Confirmation time of day’ filter allows you to narrow down data further based on the specific confirmation time of day.This complete filtering ensures that you have full control over the data you wish to analyze, providing you with targeted and relevant results.

Statistics

Upon initialization of the application, two rows of essential statistics will be displayed at the top of the interface. These statistics figures offer a complete yet comprehensive overview of the results of the applied filters.

The upper row presents statistics derived from the primary filters, which include ‘Instrument’, ‘Session’, and ‘Period’. These metrics provide a broad overview of historical price action against the Opening Balance based on your selected filters.

The lower row, on the other hand, takes your data analysis a step further. Here, the statistics are based not only on the ‘Instrument’, ‘Session’, and ‘Period’ filters but also include the ‘Confirmation time of day’. This added layer of filtration enables a more granular understanding of the market dynamics during your specified timeframes.

*Please note that any additional filtering options selected beyond these will not impact the statistics displayed in these two rows.

Data Visualisation

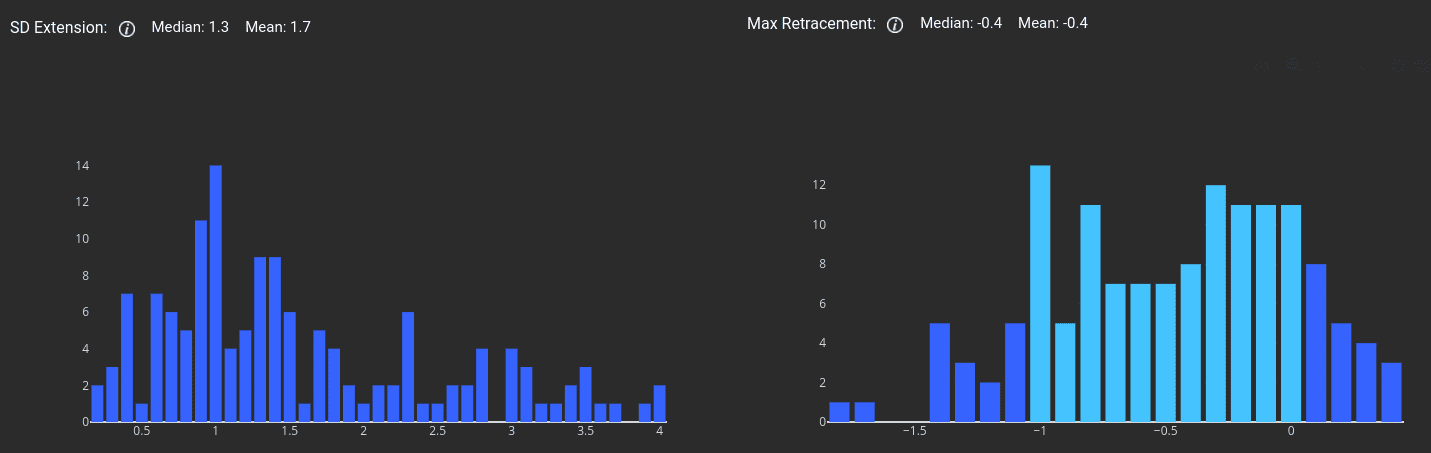

Here is where you can visualise historical price action against the Opening Balance based on your filtering. In this instance we are looking at the Max Standard Deviations for price extension and price retracement. The ‘median’ and ‘mean’ standard deviations are shown in the labels above. The mode will be the tallest bar in the sample.

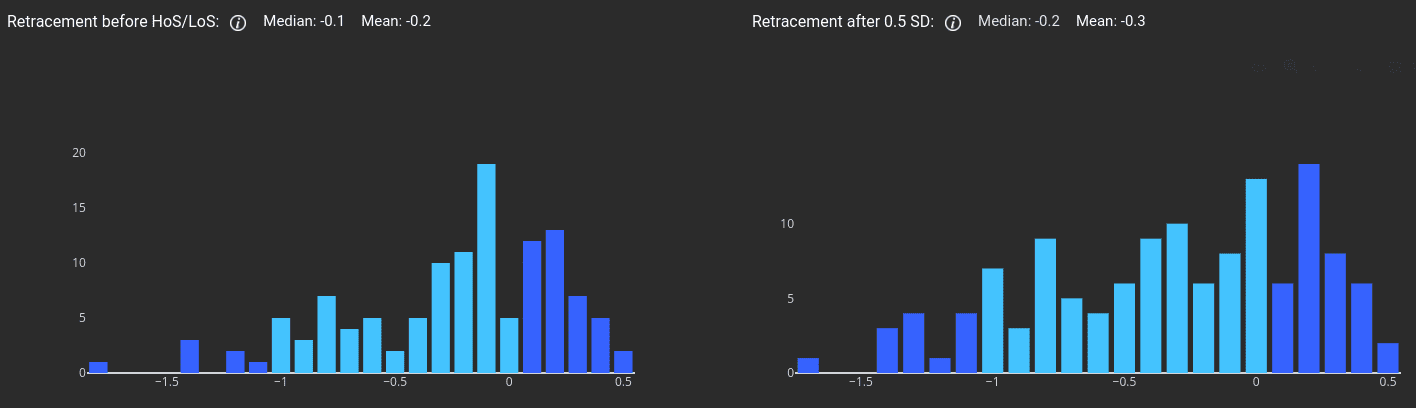

Here on the left we have Max Standard Deviation retracement before the high of session for a long and low of session for a short. On the right, we have the Maximun Standard Deviation retracement after price reached the 0.5 standard deviation extension. The ‘median’ and ‘mean’ standard deviations are shown in the labels above. The mode will be the tallest bar in the sample.

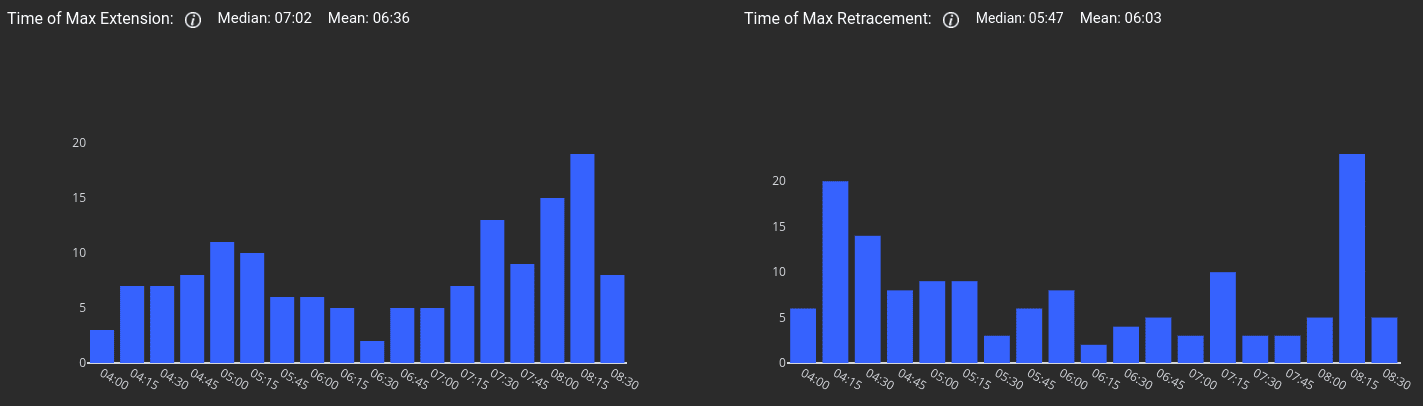

This is the distribution of Extension and Retracement times. Again the ‘median’ and ‘mean’ are displayed in the labels and the mode is represented by the tallest bar.

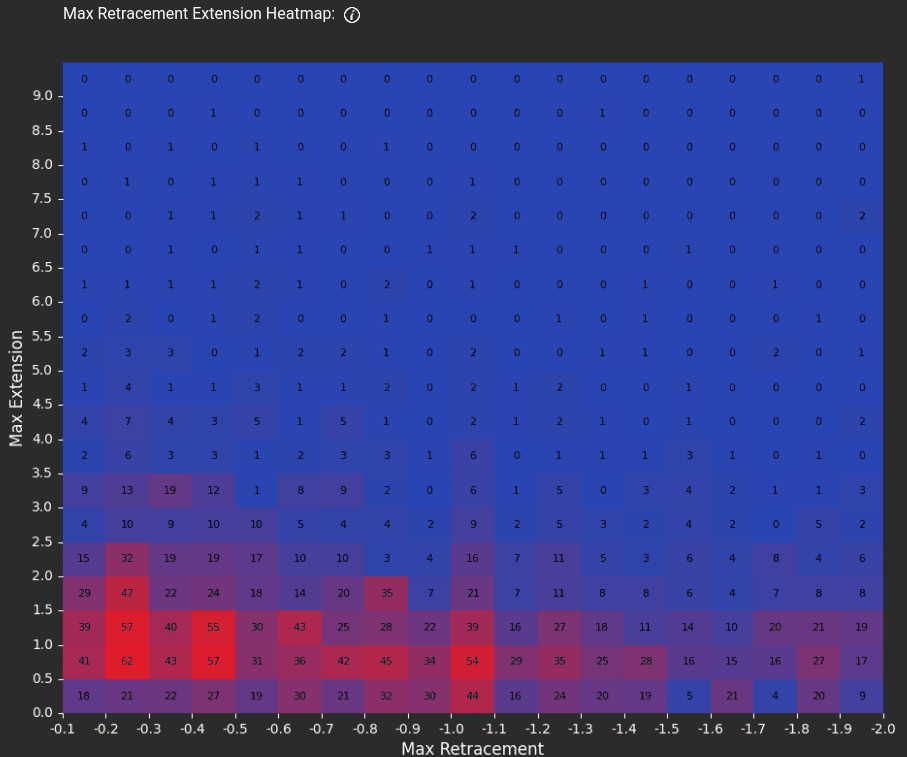

This is the heatmap showing the concentration of given price extensions for given price retracements